Most homeowners assume that when a contractor offers financing, the contractor is somehow lending their own money. That assumption leads to confusion, hesitation, and missed opportunities. Understanding what is a contractor financing option actually means changes the picture entirely. It is a point-of-sale loan product arranged through a specialist lending partner, not the contractor's personal bank account. The contractor simply connects you to the lender during the signing process. You get a fast approval, flexible payment terms, and the ability to start your renovation or home addition without draining your savings.

Table of Contents

- Key takeaways

- What is a contractor financing option and how it works

- Types of contractor financing options

- Benefits and risks of contractor financing

- How contractors and financing partners work together

- Practical tips for using contractor financing wisely

- My honest take on contractor financing after 25 years in construction

- Start your project now with PRO Construction's financing options

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Contractor financing is lender-driven | The contractor connects you to a lending partner; they never lend their own money. |

| Approval happens at signing | You apply on a phone or tablet during contract signing, often with a soft credit pull. |

| Promotional 0% periods are powerful | Paying off the balance within the promo window means you pay zero interest. |

| Carrying a balance past promo costs you | Missing the payoff deadline converts the loan to a higher-interest installment loan. |

| Compare before you commit | Always check contractor financing terms against personal loans and HELOCs before signing. |

What is a contractor financing option and how it works

The simplest way to understand contractor financing is to think of it as a point-of-sale loan. When you sit down to sign your construction contract, the contractor presents financing options through a lending partner. You fill out a short application, often on a tablet or phone, right there at the table. The lender runs a soft credit pull for pre-qualification, which does not affect your credit score. If approved, you sign a loan agreement and the project moves forward.

The loan approval process works like this: the financing company handles all underwriting, credit checks, and loan servicing. Once work is completed or reaches a milestone, the lender pays the contractor directly. You never write a check to the contractor for the financed amount. Instead, you make monthly payments to the lending company according to your agreed terms.

Here is what typically happens at each stage:

- Pre-qualification: Soft credit pull with no score impact, takes a few minutes

- Application: Completed digitally during or just after contract signing

- Approval: Often same day, sometimes within minutes

- Contractor payment: Lender pays the contractor directly after work completion or milestones

- Your payments: Monthly installments to the lender, not the contractor

Typical loan terms include promotional 0% interest periods ranging from 12 to 24 months. This means if you pay the full balance within that window, you pay no interest at all. That is a genuinely strong deal for a $20,000 kitchen remodel or a $35,000 home addition.

Pro Tip: Ask the lender specifically whether the 0% period is "same as cash" or deferred interest. With deferred interest, unpaid balances at the end of the promo period trigger all the accrued interest retroactively. With true same as cash, you only pay interest on whatever remains after the promo period ends.

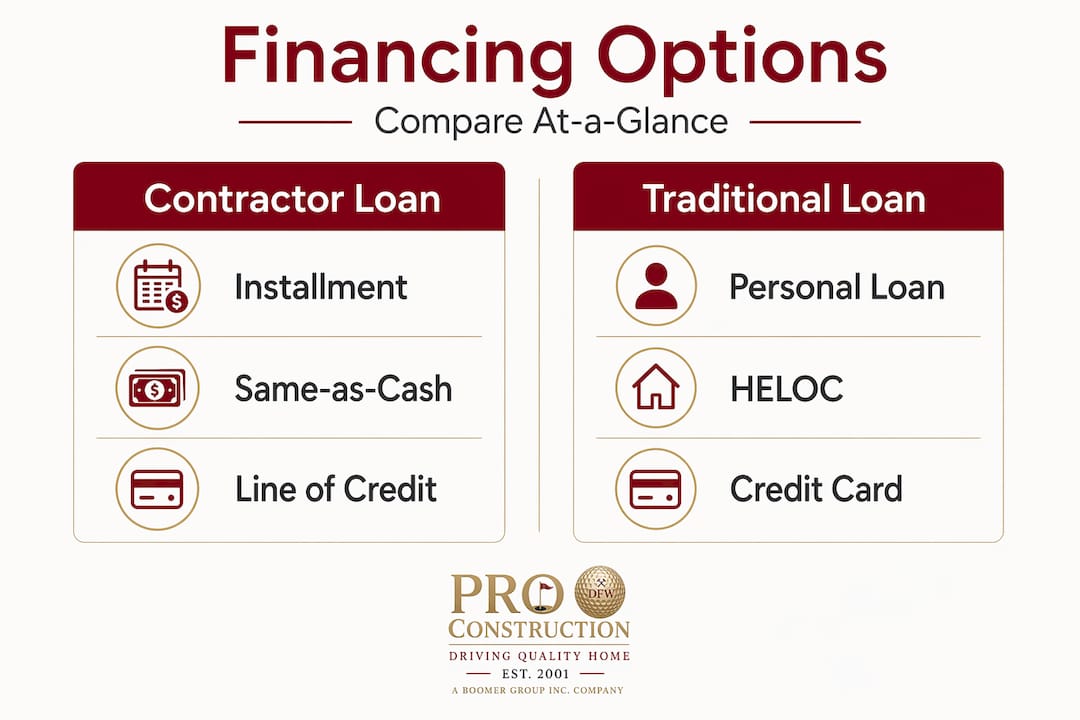

Types of contractor financing options

Not every financing product works the same way, and the right fit depends on your project size, timeline, and financial situation. Here are the main types you will encounter.

Point-of-sale installment loans are the most common. These are fixed-term loans arranged at signing, often with promotional same-as-cash offers. They work well for single, defined projects like a room addition, garage build, or bathroom remodel.

Same-as-cash loans deserve their own explanation. These offer a no-interest, no-payment promotional period. If you repay the full balance before the period ends, you owe zero interest. If you do not, accrued interest gets added to your balance, sometimes at rates above 20% APR. The upside is significant. The risk is real.

Construction lines of credit are better suited for larger or ongoing projects where costs are phased over time. You draw funds as needed and pay interest only on what you use. These are more common for property investors managing multiple renovations simultaneously.

Here is a direct comparison to help you decide:

| Feature | Contractor financing | Personal loan | HELOC |

|---|---|---|---|

| Approval time | Minutes to same day | 1 to 5 days | 2 to 6 weeks |

| Home equity required | No | No | Yes |

| Typical APR | 0% promo, then 18-26% | 8-20% | 7-12% |

| Application location | At contractor signing | Online or bank | Bank or credit union |

| Tax deductible interest | No | No | Sometimes |

| Fees | Varies by lender | Origination fee possible | Closing costs |

The right financing choice genuinely depends on your project needs and repayment timeline. A homeowner who can pay off a $15,000 addition within 18 months benefits enormously from a 0% promo loan. A property investor tackling a $120,000 multi-phase renovation might be better served by a HELOC or construction line of credit.

Pro Tip: If you have solid home equity and a longer repayment horizon, a HELOC typically offers lower long-term interest costs than contractor financing carried past its promo period. Use contractor financing when you can commit to paying it off fast.

Benefits and risks of contractor financing

The benefits are real and worth understanding clearly.

Speed and convenience top the list. You do not need to visit a bank, gather months of financial documents, or wait weeks for approval. The entire process happens during your contractor meeting. For homeowners who want to start a project before the busy season or before a family event, this speed matters.

No home equity required is a major advantage over HELOCs and home equity loans. If you are a newer homeowner or have not built significant equity yet, contractor financing gives you access to project funds without putting your home on the line as collateral.

Promotional 0% interest periods can make contractor financing the cheapest money available, provided you use it correctly. Paying off a $25,000 garage build over 18 months at 0% interest saves you thousands compared to a personal loan at 15% APR.

The risks deserve equal attention:

- Deferred interest traps: Missing the payoff window on same-as-cash loans is the single biggest risk. The loan converts to high-interest installment debt, often retroactively adding all the interest you thought you had avoided.

- Inflated contractor pricing: Some contractors build a margin into their pricing to cover the cost of offering financing. Always get at least two quotes and compare total project costs, not just monthly payments.

- Loan term confusion: Some homeowners sign without fully reading the payoff schedule. Know your exact promo end date and the interest rate that kicks in afterward.

- Budget overextension: Monthly payments that seem manageable can strain your budget if the project runs over or other expenses arise. Build a buffer.

The flexibility of payment plans is a genuine benefit for most homeowners. Spreading a $30,000 renovation over 24 months at 0% interest is far easier to absorb than writing one large check upfront.

How contractors and financing partners work together

Understanding the roles involved removes a lot of confusion about how this process actually functions.

Contractors do not lend money and they do not underwrite loans. Their role is to present financing options during the sales process, help you complete the application, and connect you with the lending partner. The contractor's estimate becomes the project cost. Everything else, including credit checks, approvals, and loan servicing, is handled entirely by the lender.

Here is how the responsibilities break down:

- Contractor's role: Present financing options, assist with application, complete the project, receive payment from lender

- Lender's role: Run credit checks, approve or deny applications, service the loan, handle all payment processing

- Your role: Apply, sign the loan agreement, make monthly payments to the lender

One practical detail worth knowing: funds are deposited directly to contractors within 24 hours of approval in many programs. That speed keeps projects on schedule and eliminates the cash flow delays that can cause contractors to slow down or pause work.

The paperless, mobile application process also matters more than it sounds. Financing programs that integrate into the sales process help contractors close jobs faster and keep projects moving. For you as a homeowner, it means less friction and a faster start date.

Practical tips for using contractor financing wisely

Before you sign anything, work through this checklist.

- Ask about the exact promo period. Get the specific end date in writing, not just "12 months." Know whether it is same-as-cash or deferred interest.

- Compare the APR after the promo period. If you think there is any chance you will carry a balance, the post-promo rate matters enormously.

- Check your credit before applying. Knowing your score helps you understand what terms to expect and whether a personal loan or HELOC might offer better long-term rates.

- Calculate total repayment cost. Multiply your monthly payment by the number of months. Then compare that number to the project cost. The difference is your interest.

- Verify the contractor's pricing is fair. Offering clear financing choices is a sign of a reputable contractor. If the total project cost seems higher than competing quotes, ask directly whether financing fees are built into the price.

- Plan your payoff strategy before signing. If you intend to use the 0% promo period, set up automatic payments or a savings plan on day one. Do not leave it to chance.

- Keep all documentation. Save copies of the loan agreement, the promo period terms, and every payment receipt. Disputes are rare but documentation protects you.

Pro Tip: Before committing to contractor financing, spend 20 minutes getting a personal loan quote from your bank or credit union. If your credit is strong and the project timeline is long, a personal loan at 9% APR might cost less than contractor financing at 0% for 12 months followed by 24% APR.

My honest take on contractor financing after 25 years in construction

I have seen homeowners pass on genuinely good projects because they assumed financing was complicated, slow, or only for people with financial trouble. That hesitation costs them. A well-structured contractor financing option is one of the most practical tools available for getting a real project started without waiting years to save the full amount.

What I have also seen, though, is homeowners sign up for same-as-cash loans without a real plan to pay them off. They hit month 13 and suddenly owe all the interest they thought they had avoided. That is not the lender's fault. It is a planning failure, and it is completely preventable.

My advice is straightforward. Use contractor financing when you have a defined project, a realistic payoff plan, and a contractor you trust to price fairly. Do not use it as a way to afford a project that is genuinely outside your budget. Financing a project you cannot repay within the promo period is not a deal. It is a debt trap dressed up as a promotion.

The homeowners I have worked with who get the most value from financing are the ones who treat the promo period like a deadline, not a suggestion. They set up their payments on day one, track the balance monthly, and pay it off with two months to spare. That discipline is what separates a smart financing decision from an expensive mistake.

— PRO

Start your project now with PRO Construction's financing options

PRO Construction has spent over 25 years helping North Texas homeowners build additions, garages, and renovations that genuinely add value to their properties. We work with trusted financing partners to make sure you can start your project sooner, without waiting until you have saved every dollar upfront.

Whether you are planning a home addition in Keller or a custom garage build, our team walks you through financing options that fit your budget and timeline. We are transparent about pricing, clear about loan terms, and committed to making sure you understand every step before you sign. Our top 1% BuildZoom ranking reflects the trust homeowners place in us, and our financing partnerships are part of how we keep projects moving from day one. Reach out to PRO Construction today and find out how affordable your next project can actually be.

FAQ

What is a contractor financing option exactly?

A contractor financing option is a point-of-sale loan arranged through a lending partner during your contract signing. The lender approves the loan, pays the contractor, and you repay the lender in monthly installments.

Does the contractor lend me the money directly?

No. Contractors do not lend money or underwrite loans. They connect you to a financing partner who handles all credit checks, approvals, and loan servicing.

What happens if I don't pay off a same-as-cash loan in time?

If you carry a balance past the promotional period, the loan converts to an interest-bearing installment loan and accrued interest gets added to your balance, often at rates above 20% APR.

How fast can I get approved for contractor financing?

Many programs offer same-day or even same-session approvals. Some lenders deposit funds to contractors within 24 hours of approval, keeping your project on schedule.

Is contractor financing better than a personal loan or HELOC?

It depends on your credit, project size, and repayment timeline. Contractor financing wins when you can pay off within the 0% promo period. A HELOC or personal loan may cost less overall if you need a longer repayment window or have strong home equity.

Recommended

- Residential Construction Contracts: A Homeowner’s Guide for Keller & North Texas - PRO Construction

- Home Addition Contractor in Keller, TX: The 2026 Homeowner’s Buying Guide - PRO Construction

- Design Build Project Management: The Homeowner’s Guide to Stress-Free Construction - PRO Construction

- How to Choose a Structural Renovation Contractor in Fort Worth TX: A Homeowner’s Guide - PRO Construction