Contractor insurance is the legal and financial protection that shields homeowners and property developers from liability, repair costs, and lawsuits when something goes wrong during a construction project. General liability, workers' compensation, and completed operations coverage are the three pillars every homeowner should understand before signing a contract. In 2026, construction claim costs are rising and insurance demands are stricter than ever, making contractor insurance necessity a non-negotiable part of any responsible building decision. Whether you are adding a room, building a garage, or undertaking a major renovation, understanding why contractor insurance matters could save you tens of thousands of dollars.

Why contractor insurance matters for protecting your investment

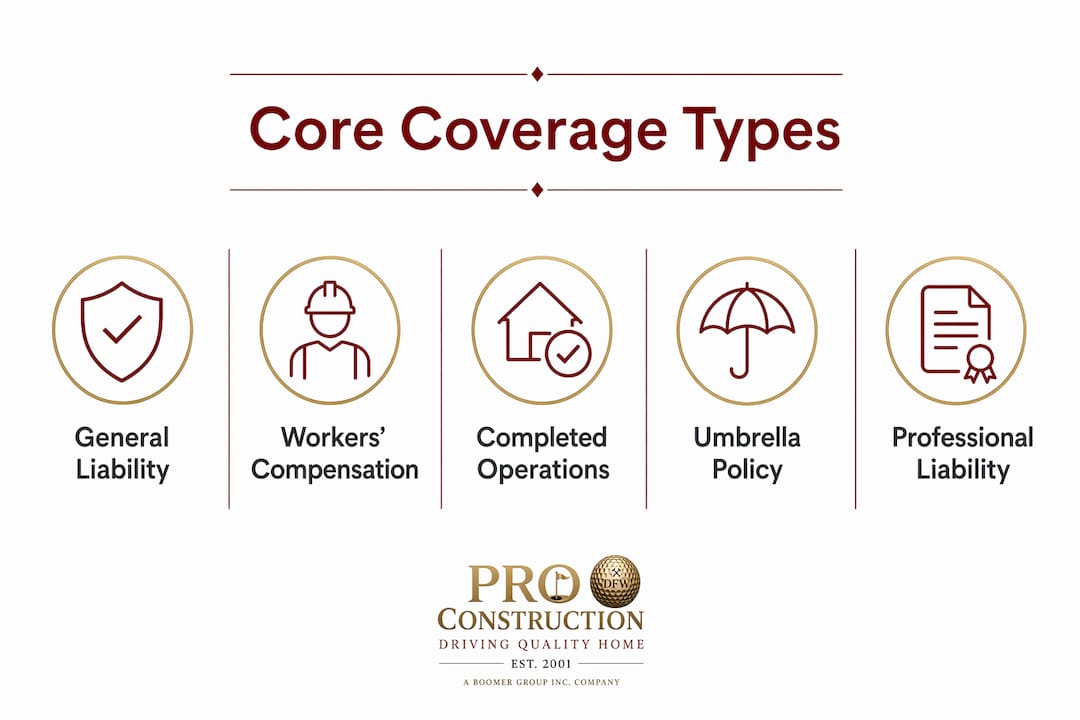

Contractor insurance is not a single policy. It is a collection of coverage types, each designed to address a specific category of risk that appears on a construction site. Knowing which policies your contractor carries tells you exactly how protected your property and finances are before a single nail is driven.

The core coverage types every homeowner should know

General Liability (GL) is the foundation. It covers third-party bodily injury and property damage caused by the contractor's work. Standard minimum GL coverage is typically $1 million per occurrence and $2 million aggregate, though larger projects often require $2 million per occurrence and $4 million aggregate. That minimum matters because a single slip-and-fall lawsuit can easily exceed $500,000 in legal fees and settlements.

Workers' Compensation covers medical bills and lost wages for any contractor employee injured on your property. Workers' comp is legally required in nearly every state once a contractor hires even one employee. Without it, you as the property owner can be held personally liable for an injured worker's costs. Monthly premiums range from $77 to over $400 depending on the contractor's risk profile, which is a small price compared to the exposure it eliminates.

Completed Operations coverage protects against claims that surface months or even years after the project ends. A faulty pipe installation that causes water damage six months later is a completed operations claim, not a general liability claim. Neglecting this coverage leaves both the homeowner and the contractor exposed to delayed, expensive disputes.

Beyond these three, umbrella liability policies extend coverage beyond standard limits. Umbrella policies cost roughly $300 to $600 per year for $1 million in additional coverage, making them one of the most cost-effective ways to handle catastrophic claims. Surety bonds and commercial auto policies round out a contractor's full coverage picture.

| Coverage Type | What It Protects |

|---|---|

| General Liability | Third-party injury and property damage during the project |

| Workers' Compensation | Medical and wage costs for injured contractor employees |

| Completed Operations | Claims arising after project completion from installation errors |

| Umbrella Liability | Coverage beyond standard GL and workers' comp limits |

| Commercial Auto | Vehicles used for work, not covered by personal auto policies |

Annual costs for contractor insurance vary significantly by trade. A solo handyman typically pays $2,000 to $5,000 per year. A general contractor with a crew pays $5,000 to $15,000. Roofers, who carry higher physical risk, pay $8,000 to $25,000. These figures reflect real risk exposure, and a contractor who cannot afford or refuses to carry proper insurance is a contractor whose risk is being transferred directly to you.

How contractor insurance protects you from financial and legal risk

The practical benefits of contractor insurance go well beyond abstract protection. They show up in specific, costly scenarios that homeowners encounter more often than most realize.

Here are the four most common ways contractor liability coverage directly protects your finances and legal standing:

-

Accident liability on your property. If a contractor's employee is injured on your job site and the contractor has no workers' comp, your homeowner's insurance may be forced to respond. Depending on your policy, that could mean a claim that raises your premiums or exceeds your coverage limits entirely.

-

Property damage caused by the contractor. A crew that accidentally damages a neighboring fence, a parked car, or your existing structure creates a liability. GL coverage pays for those repairs. Without it, you may need to pursue the contractor personally, which means litigation.

-

Lawsuit costs from third parties. A visitor who trips over construction debris and sues can name both the contractor and the property owner. GL coverage funds the contractor's legal defense and any settlement, keeping your personal assets out of the equation.

-

Project delays from uninsured incidents. When an uninsured contractor faces an injury claim or property dispute, work stops. Legal proceedings take months. The financial and timeline cost to you as the property owner can dwarf the original project budget.

Pro Tip: Before any contractor sets foot on your property, ask for a Certificate of Insurance and call the issuing insurer directly to confirm the policy is active. A certificate can be outdated or fraudulent, and a two-minute phone call eliminates that risk entirely.

Proof of insurance is often a mandatory condition before contractors can access a job site. This is not bureaucratic formality. It is the first line of defense for your investment. Contractors who resist providing documentation are signaling that their coverage may be inadequate or nonexistent.

Why verifying and customizing contractor insurance matters for your project

Holding a certificate of insurance is not the same as being properly protected. The details inside that certificate determine whether you are actually covered when a claim occurs.

Here is what to check before work begins:

- Additional insured endorsement. This adds you, the property owner, directly to the contractor's GL policy. Without it, the contractor's insurer has no obligation to defend or indemnify you in a shared claim.

- Waiver of subrogation. This prevents the contractor's insurer from suing you to recover money it paid out on a claim. These endorsements must be arranged before work starts. Attempting to add them mid-project causes delays or disqualification from the contract entirely.

- Coverage limits matched to project scope. A $500,000 home addition carries different risk than a $15,000 deck repair. The contractor's coverage limits should reflect the scale and complexity of your specific project.

- Exclusions relevant to your project type. Some GL policies exclude certain trades, materials, or work locations. A contractor specializing in roofing may carry a policy that excludes foundation work if they attempt it.

- Policy expiration dates. A policy that expires mid-project leaves you unprotected for the remainder of the build. Confirm coverage runs through the projected completion date, with buffer.

Coverage must be tailored to specific project risks and contract requirements. A generic policy is often inadequate, and many contractors do not realize their standard coverage excludes the exact scenario that causes a claim. As a homeowner, you cannot assume the contractor has handled this correctly. You need to verify it yourself.

Pro Tip: Ask your contractor for a copy of their full policy declarations page, not just the certificate. The declarations page shows exact coverage limits, exclusions, and endorsements in plain language. Any reputable contractor will provide this without hesitation.

Reviewing a contractor's license and insurance together gives you the most complete picture of their legitimacy. In Texas, both licensing and insurance requirements vary by trade and municipality, so confirming both protects you on two fronts simultaneously.

Common misconceptions about contractor insurance coverage

Several widespread misunderstandings lead homeowners to assume they are protected when they are not. Clearing these up before you hire is far less expensive than discovering them during a claim.

| Misconception | Reality |

|---|---|

| GL insurance is legally required everywhere | GL is not universally mandated by law, but most contracts and job sites require it as a condition of access |

| Workers' comp is optional for small crews | Workers' comp is required in nearly every state once a contractor has even one employee |

| GL covers faulty workmanship | GL covers physical damage and bodily injury. Professional errors require a separate Professional Liability policy |

| Personal auto covers work trucks | Personal auto policies rarely cover vehicles used for work. A commercial auto policy is required |

| Completed operations is included automatically | Many contractors carry GL without completed operations, leaving post-project claims entirely uncovered |

The faulty workmanship exclusion catches homeowners off guard most often. If a contractor installs windows incorrectly and water damage appears two years later, GL alone will not cover the repair. Completed operations coverage is the policy that responds to those delayed claims, and it must be explicitly included. Many contractors overlook it entirely, which is why you need to ask for it by name.

The professional liability gap is equally significant. A contractor who designs a structural element incorrectly and causes damage is creating a professional error, not a physical accident. That distinction means GL pays nothing. Errors and Omissions coverage, also called Professional Liability, is the correct policy for that scenario. For design-build projects, confirming this coverage is non-negotiable.

Understanding contractor licensing requirements alongside insurance gaps gives you a complete picture of the risks you face when hiring without proper verification.

Key takeaways

Contractor insurance protects homeowners and property developers from personal liability, repair costs, and project delays caused by uninsured incidents on their construction sites.

| Point | Details |

|---|---|

| Core coverage types | General Liability, Workers' Comp, and Completed Operations are the three policies every homeowner must confirm. |

| Verify before work starts | Request a Certificate of Insurance with additional insured endorsement and waiver of subrogation before any work begins. |

| Generic policies create gaps | Coverage must match the project's scope, trade, and location. A standard policy often excludes the exact risk that causes a claim. |

| Completed operations is often missing | Many contractors omit this coverage, leaving homeowners exposed to claims that surface months or years after project completion. |

| Insurance signals professionalism | Contractors who carry proper, documented insurance win better contracts and protect their clients more effectively. |

What 25 years of construction projects taught me about insurance

After more than two decades working on home additions and garage builds across North Texas, the pattern is clear. The homeowners who face the worst outcomes are almost never the ones who hired the most expensive contractor. They are the ones who hired the cheapest contractor and never asked about insurance.

I have seen projects stall for months because an uninsured worker was injured and the homeowner's own policy was dragged into the dispute. I have seen property owners receive repair bills for damage caused by a contractor who had no GL coverage and simply disappeared. These are not edge cases. They happen regularly, and they are entirely preventable.

Insured contractors signal something beyond legal compliance. They signal that they have enough professional standing to qualify for coverage, that they operate transparently enough for an insurer to underwrite them, and that they take their clients' financial exposure seriously. When a contractor resists showing you their certificate, that resistance is information. Use it.

The homeowners I respect most treat insurance verification the same way they treat reviewing a bid. They do it before committing, they ask specific questions, and they walk away from contractors who cannot answer those questions clearly. That habit has protected more investments than any contract clause ever written.

— PRO Construction

Build with confidence using PRO Construction's insured services

PRO Construction has served North Texas homeowners for over 25 years with fully insured home addition and garage building services. Every project PRO Construction undertakes is backed by proper General Liability, Workers' Compensation, and Completed Operations coverage, so your investment is protected from day one through project completion and beyond. PRO Construction holds a top 1% ranking on BuildZoom, reflecting a track record of quality craftsmanship and transparent project management that clients can verify before signing anything.

If you are planning a home addition or garage build in the Keller or Fort Worth area, explore insured home addition services or check out PRO Construction's garage building options. Ask about current discounts when you reach out.

FAQ

What is contractor insurance and why do homeowners need it?

Contractor insurance is a set of policies, including General Liability, Workers' Compensation, and Completed Operations coverage, that protect both the contractor and the property owner from financial losses caused by accidents, injuries, and property damage during a construction project. Homeowners need it because without it, they can be held personally liable for incidents that occur on their own property.

How do I verify that a contractor's insurance is valid?

Request a Certificate of Insurance before work begins, then call the issuing insurer directly to confirm the policy is active and includes the correct endorsements, such as additional insured status and waiver of subrogation. A certificate alone is not sufficient verification since policies can lapse or be misrepresented.

Does general liability insurance cover faulty workmanship?

General Liability does not cover professional errors or faulty workmanship. It covers physical damage and bodily injury caused by the contractor's operations. Errors in design or installation require Professional Liability coverage, and post-completion damage from installation errors requires Completed Operations coverage.

Is workers' compensation required for contractors in Texas?

Texas is the only state that does not mandate workers' compensation for private employers, but most general contractors and project owners require it as a contract condition. Without it, an injured worker can sue the property owner directly, making it a practical necessity even where it is not legally required.

What happens if I hire an uninsured contractor?

If an uninsured contractor causes property damage or an employee is injured on your site, you as the property owner may be held financially responsible for repair costs, medical bills, and legal fees. Your homeowner's insurance may respond, but coverage limits and policy exclusions can leave significant gaps in your protection.